Israel Excluded from the Global Tech Recovery; Amid unprecedented geopolitical turmoil, the Israeli tech sector underperformed compared to the U.S.; Cyber and Healthcare sectors gained market share, surpassing IT technology companies; The positive trend is expected to continue in 2025, but Israel remains in waiting mode.

The Israeli tech sector showed relative weakness in 2024. Due to the ongoing war, credit rating downgrades, and difficulties with attracting foreign investors, it detached from the U.S. trend for the first time in years. According to research conducted by S Cube, a firm specializing in high-tech company valuations, while U.S. companies began recovering from the deep crisis that had affected the global tech sector, Israeli tech firms, which were subjected to the negative impact of the ongoing war on the economy, continued with their negative moment from last year. Additionally, demand for investments in the Cyber sector returned. Examining the sector’s investment volumes, although the overall amount of capital flowing into the tech sector significantly declined in 2024, the few companies that managed to raise funds benefited from an increase in the median investment amount compared to last year.

Due to the Conflict, Israel Was Excluded from the Global Tech Recovery

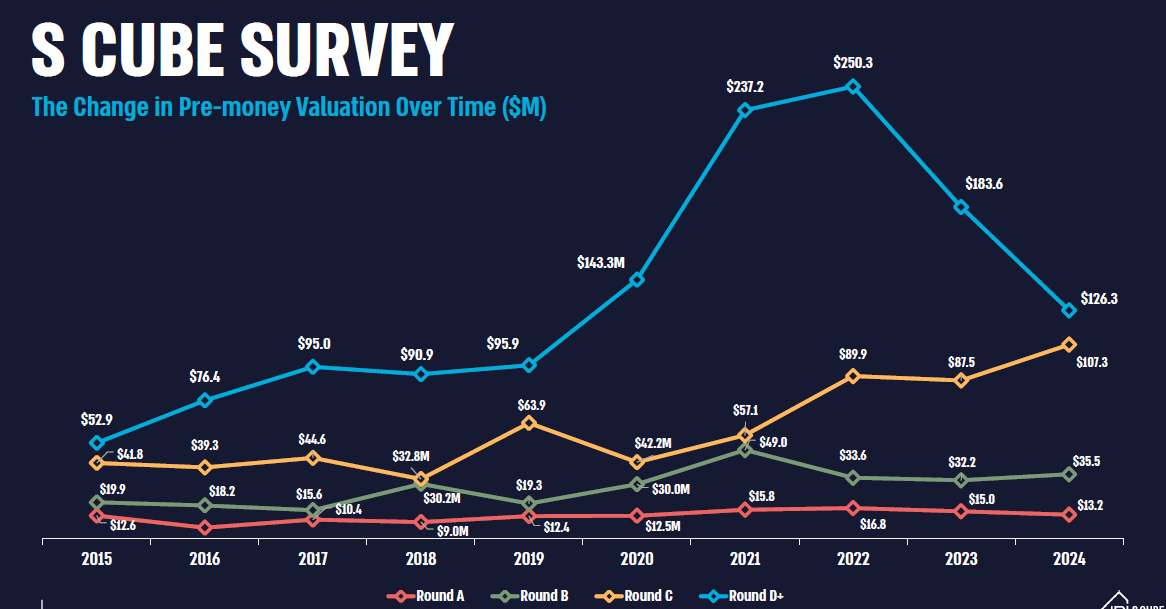

Based on data from thousands of valuations performed by S Cube since 2013, despite the recovery recorded in the global technology sector last year, geopolitical events in Israel led to a significant 26% drop in the number of funding rounds. Among the rounds that did take place, there was a 31% decrease in the median valuation for advanced-stage rounds (Series D and above) compared to last year, whereas Series C rounds saw a 23% increase in median valuation. Early-stage rounds exhibited mixed trends, with a 10% rise in median valuations for Series B rounds, but a 12% drop in early-stage round valuations. Moreover, last year’s funding rounds often included improved terms for investors, such as granting warrants or applying a multiplier greater than one on guaranteed investment returns. These elements further reduced company valuations economically but are not reflected in reported valuations due to technical reasons.

Considering the challenging year for Israel’s economy and technology sector, the performance of Israeli tech firms relative to the U.S. became a cause for concern. In comparison, during the first three quarters of last year, the median valuation for advanced-stage companies (Series C and above) in the U.S. increased by 46%, whereas in Israel, the median valuation for these companies dropped by 15%. While the median valuation for Series B rounds in the U.S. soared by 96%, it increased by only 10% in Israel. For early-stage rounds, the median valuation rose by 11% in the U.S. but declined by 12% in Israel.

In previous years, trends in Israel were less pronounced compared to the U.S. but followed a similar directional pattern. That is, during boom times, U.S. valuations rose at higher rates, and during downturns, they fell more sharply. However, in the past year, due to the ongoing conflict, a concerning trend emerged where the Israeli tech sector diverged from the U.S. The primary reason for this phenomenon is the increased risk premium attributed to companies with Israeli ties and the uncertainty caused by the ongoing war. Factors such as Israel’s credit rating downgrades, foreign investors’ reluctance to visit Israel, declining national morale, and capital outflows further exacerbated the situation.

Few Companies Secured Funding, but Investment Sizes Increased

Examining funding volumes last year, after two consecutive years of double-digit declines in median investment for advanced-stage rounds (Series D and above), 2024 saw relative stability, with only a 2% decrease in median investment, reaching $30 million compared to $30.7 million last year. Encouragingly, other segments of the sector showed positive trends in investment volumes, including a 75% rise in median Series C investment to $17.5 million (compared to $10 million last year), a 118% surge in median Series B investment to $16.1 million (compared to $7.4 million last year), and a modest 7% increase in median early-stage investment to $6.2 million (compared to $5.8 million last year). While this trend may be misleading given the sector’s challenging year, it underscores the principle that high-potential companies continue to advance even during crises.

When the Guns Roar, Cyber Demand Soars

Despite the turmoil in the tech sector, the technological revolution has not slowed, and demand for technology continues to grow and expand into new industries. The leading sectors remained unchanged from the previous year. However, Cyber emerged as the most prominent sector in 2024, accounting for approximately 30% of all funding rounds, up from 19% in 2023, when it ranked second.

The second most prominent sector was Healthcare and Life Sciences, which accounted for 22% of funding rounds, compared to 16% last year. This sector includes pharmaceuticals, medical equipment, digital health, and biotechnology.

The third-largest sector in 2024 was IT & Enterprise Software, which led in the previous two years. It accounted for 25.5% of rounds in 2023 and 33% in 2022 but only 15% in 2024. This sector, which includes artificial intelligence-based technologies aimed at improving business performance, slightly outperformed the Fintech and InsurTech sector, which accounted for 10% of funding rounds last year.

Positive Momentum Expected in 2025, but Israel Remains in Waiting Mode

Globally, we expect the positive trend in the tech sector to continue in 2025. Following a slowdown in IPOs last year, the number of tech IPOs is expected to rise. The volume of capital seeking investment remains massive, and with anticipated interest rate cuts in the U.S., demand for venture capital and startup investments is expected to grow. In contrast, in the Israeli market, geopolitical uncertainty was the primary reason for the sector’s divergence from the U.S. trend. While there has been some progress, including a ceasefire agreement with Hamas, uncertainty remains high and will likely continue to affect the Israeli economy in 2025. Consequently, capital outflows from Israel will likely persist unless there is a major improvement in the geopolitical situation.

This article is for informational purposes only and does not constitute “investment advice” or “investment marketing” as defined by the Investment Advice, Investment Marketing, and Portfolio Management Law, 1995, nor does it serve as a substitute for such advice or for legal, financial, tax, economic, or other professional consultation. S-Cube, IBI Group, or any of its affiliates shall not be liable for any loss or damage incurred by third parties based on reliance on the above information.